The 4-Bucket Retirement Strategy: Using Home Equity and Reverse Mortgages to Reduce Retirement Portfolio Risk

Featured Insight

One of the biggest threats to retirement success is not necessarily poor long-term investment returns—it is poor timing. Research from retirement income specialists including Wade D. Pfau, Ph.D., CFA, Barry Sacks, Ph.D., and Stephen Sacks, Ph.D., suggests that coordinated use of home equity through a reverse mortgage line of credit may significantly reduce retirement portfolio exhaustion risk.

Retirement Planning Has Changed

Traditional retirement planning focused heavily on accumulating investment assets.

But retirement itself is a completely different phase of life.

Once withdrawals begin, retirees become vulnerable to:

- Market volatility

- Sequence-of-returns risk

- Inflation

- Tax inefficiency

- Longevity risk

Today, many retirement researchers believe that home equity should no longer be viewed solely as a “last resort” asset.

Instead, coordinated use of home equity may become an important part of retirement income planning.

Section 1: The Sequence of Returns Risk (The Hidden Threat)

One of the greatest dangers in retirement is called sequence-of-returns risk.

This occurs when retirees experience market losses early in retirement while simultaneously withdrawing money from investment accounts.

This combination can permanently damage a portfolio’s ability to recover.

Example: Why Timing Matters

Imagine two retirees:

- Each starts retirement with $500,000

- Each withdraws $40,000 annually

- Each earns similar average long-term returns

Retiree A: Bad Timing

- Year 1: -20% market decline

- Year 2: -10% decline

- Year 3: +15% recovery

Because withdrawals continue during the downturn, the portfolio may never fully recover.

Retiree B: Better Timing

- Year 1: +15% growth

- Year 2: +10% growth

- Year 3: -20% decline

Even though the average returns are similar, Retiree B often ends retirement with substantially more money because early gains created a larger cushion.

Why This Matters

Researchers emphasize that volatility becomes far more dangerous once retirees begin distributions.

For retirees taking withdrawals, volatility becomes risk.

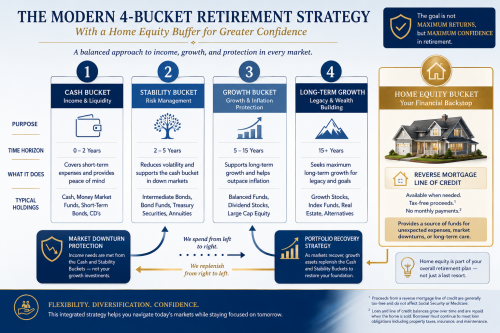

Section 2: The 4-Bucket Allocation System

The 4-Bucket Strategy organizes retirement assets based on when the money will likely be needed.

This approach may help retirees:

- Reduce emotional investing

- Avoid selling assets during downturns

- Improve retirement cash flow stability

- Coordinate portfolio withdrawals more efficiently

Bucket 1: Cash & Immediate Needs

Purpose: Cover 1–2 years of expenses.

Typical Assets:

- High-Yield Savings Accounts (HYSAs)

- Cash reserves

- Money market accounts

Goal: Avoid selling investments during market downturns.

Bucket 2: Income & Stability

Purpose: Cover approximately 3–5 years of retirement income needs.

Typical Assets:

- CDs

- Treasury bonds

- Fixed-income investments

- Conservative bond funds

Goal: Create predictable retirement income with lower volatility.

Bucket 3: Growth & Inflation Protection

Purpose: Support years 7–15 of retirement.

Typical Assets:

- Dividend-paying stocks

- ETFs

- Real estate investments

Goal: Outpace inflation and preserve purchasing power.

Bucket 4: Long-Term Growth & Home Equity Coordination

Purpose: Support long-term retirement flexibility beyond year 15.

Typical Assets:

- Growth equities

- Index funds

- Coordinated home equity strategies

- Reverse mortgage line of credit planning

Goal: Provide flexibility and help reduce portfolio stress during difficult market periods.

Why Researchers Are Reconsidering Home Equity

For decades, conventional retirement advice suggested retirees should only use home equity after exhausting investment portfolios.

However, multiple retirement research studies now challenge that belief.

Research published in the Journal of Financial Planning found that coordinated use of home equity through a reverse mortgage line of credit may significantly reduce the probability of retirement portfolio exhaustion.

The Reverse Mortgage “Buffer Asset” Strategy

One of the most important findings from the research is the idea of using a reverse mortgage line of credit as a:

Buffer Asset

Instead of withdrawing from investment accounts during major market downturns, retirees may temporarily access funds from home equity.

This allows investment portfolios more time to recover.

Reducing portfolio withdrawals during market declines may help mitigate sequence-of-returns risk.

Why Timing Matters

Research by Sacks and Sacks demonstrated that even skipping a few withdrawals from a volatile portfolio following market declines may dramatically improve long-term portfolio sustainability.

The key insight:

- Selling investments after losses locks in damage

- Alternative income sources may reduce that pressure

- Home equity can function as a non-correlated retirement asset

Section 3: The Tax-Efficient Withdrawal Sequence

Retirement success is not only about investment returns.

It is also about how withdrawals are coordinated.

Step 1: Take Required Minimum Distributions (RMDs) First

Tax-deferred accounts generally require mandatory distributions at certain ages.

These should typically be addressed first to avoid penalties.

Step 2: Use Taxable Brokerage Accounts Strategically

Taxable accounts may offer flexibility for managing:

- Tax brackets

- Capital gains exposure

- Medicare premium thresholds

Step 3: Coordinate Tax-Deferred Withdrawals Carefully

Traditional IRA and 401(k) withdrawals generally create ordinary income taxes.

Large withdrawals may unexpectedly increase tax exposure.

Step 4: Preserve Roth Accounts for Flexibility

Roth IRAs may provide:

- Tax-free withdrawals

- Future tax flexibility

- Estate planning advantages

Where Reverse Mortgages May Fit Into the Withdrawal Strategy

One major advantage of reverse mortgage proceeds:

Reverse mortgage funds are generally not taxable income.

Because reverse mortgage proceeds are loan advances rather than earned income, they may help retirees manage taxable income exposure.

This may potentially help with:

- Tax bracket management

- Medicare IRMAA thresholds

- Portfolio longevity

- Social Security taxation coordination

Section 4: The 2026 Social Security Maximization Strategy

Another major retirement planning opportunity involves delaying Social Security benefits.

Benefits may increase approximately:

8% per year

for each year benefits are delayed beyond full retirement age until age 70.

Why This Matters

Larger guaranteed lifetime income may help reduce portfolio withdrawal pressure later in retirement.

This can be especially valuable during periods of market volatility.

Coordinating Social Security, Investments & Home Equity

Modern retirement planning increasingly focuses on:

- Coordinated withdrawals

- Tax efficiency

- Guaranteed income optimization

- Home equity integration

- Longevity protection

Retirement researchers increasingly view home equity as a retirement asset—not merely an emergency asset.

Key Takeaways

- Sequence-of-returns risk can permanently damage retirement portfolios.

- The 4-Bucket Strategy organizes assets based on timing and purpose.

- Research suggests coordinated use of home equity may reduce portfolio exhaustion risk.

- Reverse mortgage line-of-credit strategies may serve as retirement “buffer assets.”

- Reverse mortgage proceeds are generally not taxable income.

- Delaying Social Security may improve long-term retirement cash flow stability.

- Retirement success often depends on coordination—not simply investment returns.

Frequently Asked Questions

What is sequence-of-returns risk?

Sequence-of-returns risk occurs when retirees experience poor market performance early in retirement while taking withdrawals from investment accounts.

How can a reverse mortgage help retirement planning?

Research suggests that coordinated use of a reverse mortgage line of credit may reduce pressure on investment portfolios during market downturns.

Are reverse mortgage proceeds taxable?

Generally, no. Reverse mortgage proceeds are typically treated as loan advances rather than taxable income.

Why do retirement researchers discuss home equity more today?

For many retirees, home equity represents one of the largest assets on the household balance sheet and may provide additional retirement flexibility.

Final Thought

Retirement planning is evolving.

The old model of relying exclusively on investment portfolios is being reconsidered as researchers explore more flexible and diversified retirement income strategies.

For many retirees, home equity may become an important component of retirement stability—not simply a last resort.

The goal is not just maximizing returns.

The goal is creating sustainable income, reducing unnecessary risk, and improving long-term financial confidence throughout retirement.

```